Protect yourself

One thing to know before this section. You're not the lawyer. You're not the financier. You don't underwrite, draft from scratch, or carry liability for either side's transaction. What you do own is making sure the right paperwork is in place before introductions happen, so neither party can cut you out. The depth below is a framework, not a daily grind — you set up clean templates once (with a lawyer's review) and reuse them for every deal.

This is where most new brokers get killed. They make the introduction. They do the work. Then the buyer and supplier take the relationship direct and cut the broker out. You never see another dollar.

You prevent this with three documents. Sign them before you introduce anyone to anyone. Every time. No exceptions.

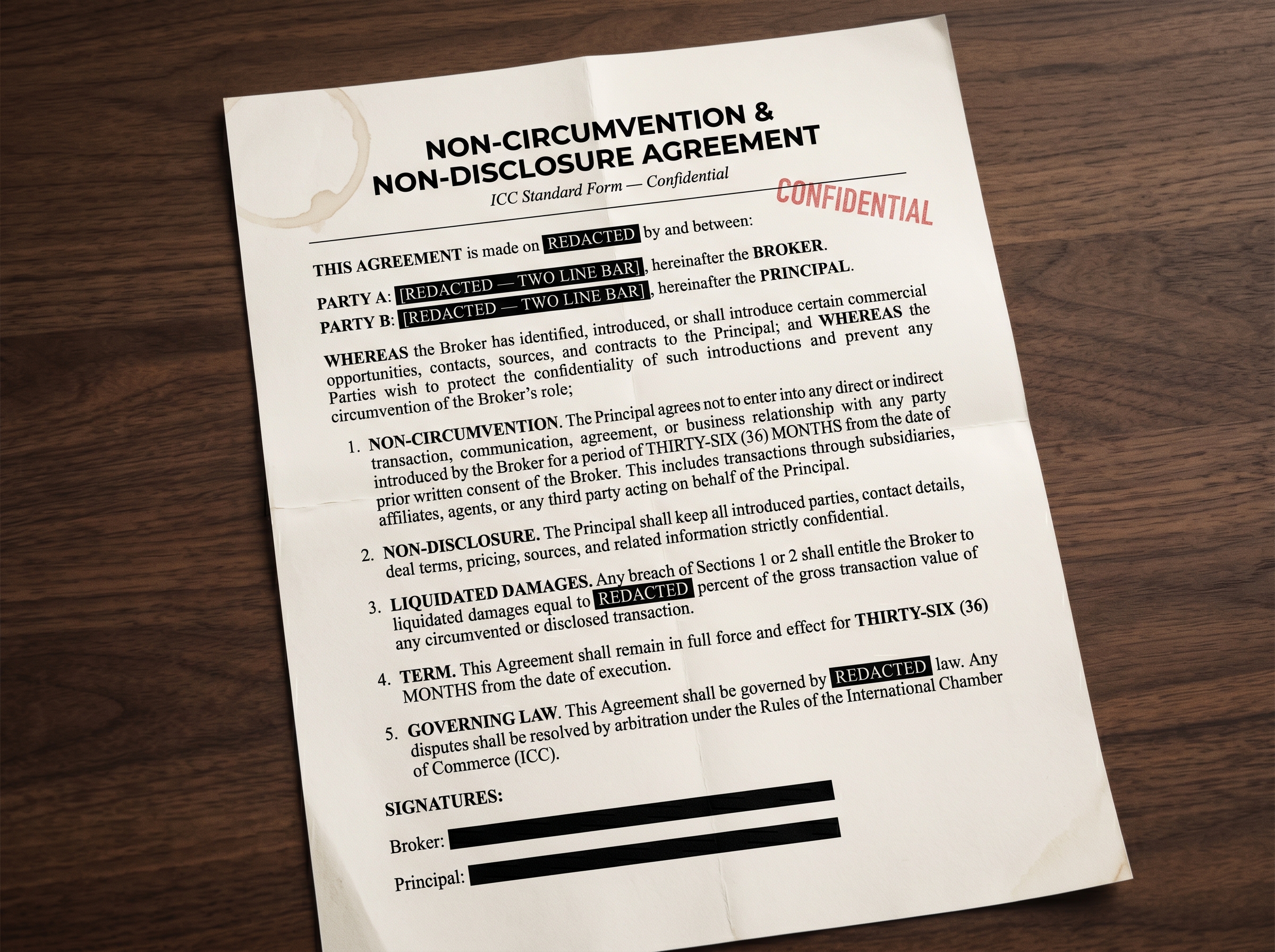

11.5.1 — NCA (Non-Circumvention Agreement)

The base layer. The parties (buyer and supplier) agree not to go around you. If they transact directly after you introduced them, they owe you damages. Typical term: three years from the date of introduction.

Key clauses to include:

- Definition of "circumvention" — both direct (cutting you out) and indirect (using subsidiaries or affiliates).

- Liquidated damages — a specific dollar amount or percentage of transaction value if circumvention occurs. Without this, you have to prove damages, which is hard.

- Term — three years is standard. Some brokers push for five.

- Jurisdiction — where disputes will be resolved. Pick somewhere with reliable enforcement (UK, US, Singapore are common defaults).

- Confidentiality — supplier and buyer agree not to share each other's identity with third parties.

11.5.2 — NCND (Non-Circumvention Non-Disclosure)

The NCA's bigger sibling. Same circumvention protection, plus confidentiality protection. The parties agree not to share your supplier (or buyer) information with any other broker, competitor, or third party.

Use NCND when:

- The supplier or buyer is in a competitive market and identity leakage is a real risk.

- You're dealing with a counterparty who routinely works with multiple brokers.

- The deal involves IP or proprietary processes (specialty manufacturing, chemical formulations).

11.5.3 — MFPA (Master Fee Protection Agreement)

The contract that locks in your commission. Specifies:

- Your commission rate (typically 5-15% depending on commodity).

- The basis for the commission (gross transaction value, net of certain costs, etc.).

- Payment terms (when and how you get paid — typically wire within X days of each transaction).

- The term over which the commission applies (typically 36 months for all transactions between the introduced parties).

- What happens if a party tries to renegotiate (you maintain rights for the original term).

The MFPA is the document that turns "introducing two parties" into "owning a percentage of a deal flow for three years." Without it, you're a finder. With it, you're a broker.

11.5.4 — The signing sequence (order matters)

Here's the actual order of operations:

- You and the buyer sign the NCA + MFPA before you mention any specific supplier.

- You and the supplier sign the NCA + MFPA before you mention any specific buyer.

- (Optional but recommended) a tri-party MFPA when both sides are introduced — locks in commission terms and provides legal recourse if either party tries to circumvent.

- Only then do you make the introduction.

This order matters because once the introduction is made, your leverage drops. Before introduction, both parties want what you have (the other party). They'll sign. After introduction, they have what they wanted (each other) and the contract becomes much harder to negotiate.

11.5.5 — Common pushback (and how to handle it)

"We don't sign agreements before knowing who you're representing."

Common from buyer side. Response: "I understand. The agreement is mutual — it protects you too. Once it's signed, I introduce you to a verified supplier in [region] who can supply [volume] at [price range]. The agreement is what makes the introduction possible." If they still refuse, they're either not serious or planning to circumvent. Either way, walk.

"Three years is too long."

Negotiate to twenty-four months as a fallback. Don't go below eighteen. If they push for under a year, they're planning to do one deal and cut you out.

"We want to use our own template."

Fine, but read it carefully. Their template will favor them. Push back on circumvention definitions, term length, and damages clauses if any of those are weaker than your version.

Where to get the templates: Standard NCA, NCND, and MFPA templates exist in ICC (International Chamber of Commerce) standard form. Search "ICC NCND template" or "ICC MFPA template." Have a lawyer review your template before you use it — a $200 review can save you a six-figure dispute. Once you have a clean template you trust, you can reuse it for every deal.

The Iron Rule of Brokering

No signed protection = no introduction. No exceptions. Not for "trusted contacts." Not for "small first deals." Not for "we'll do the paperwork next week." Every time you make an unprotected introduction, you're betting your commission against the other party's character. That's not a bet you should ever take.